It’s Oscar night and Three Billboards Outside Ebbing, Missouri is one of the favorites of nine films nominated for Best Picture. Three Billboards grossed about $123 Million, not too many folks including perhaps some Academy members have even seen the film which pundits say helps explain the complacency and continued drop in Oscar ratings due to the lack of a major blockbuster like Titanic.

It’s Oscar night and Three Billboards Outside Ebbing, Missouri is one of the favorites of nine films nominated for Best Picture. Three Billboards grossed about $123 Million, not too many folks including perhaps some Academy members have even seen the film which pundits say helps explain the complacency and continued drop in Oscar ratings due to the lack of a major blockbuster like Titanic.

In the trust and fiduciary world it seems complacency continues as well, despite several recent blockbuster announcements.

Blockbuster #1 the SEC announced the Selective Share Class Disclosure initiative, effectively a sort of voluntary amnesty for registered investment advisers who may have invested customers’ funds in high/er fee share class mutual funds and not disclosed same to investors. The initiative includes a potential refund to affected investors, so it’s best to contact your RIA. UPDATE March 11 , 2019 – The SEC announced that investors will get refunds from 79 advisers totaling $125 Million. The SEC press release is here.

The 79 firms charged are listed at the end of the SEC’s press release. If you may need assistance with obtaining, understanding or reconciling (making sure the refund is correct) a potential refund you may contact us for a rapid response to same. Our contact info is below at the end of this post or on the “Contact” page including our US mail and fax number, if that’s more convenient for you.

Investors and in particular, trustees and fiduciaries should bear in mind this announcement covered just 79 advisers (who voluntarily admitted to violations of the Investment Advisers Act) out of over 12,000 SEC-registered investment advisors and while not under the SEC’s purview, there’s over 17,000 State – registered investment advisers.

And this quote from SEC chair, Jay Clayton: and services to our retail investors, ranging from one-time advice on a model investment portfolio to comprehensive planning combined with continuous investment advice and other services. Regardless of the scope and duration of the investment advisory services, investment advisers are fiduciaries and, as such, their duties of care and loyalty require them to disclose their conflicts of interest, including financial incentives”

Note, FINRA did not ask for share class disclosures which means, at least in part, that investors with accounts at a broker dealer may wish to ask their registered representative about mutual fund share class over charges, potential refunds and or disclosures of same. And request any response for same in writing.

FINRA oversees registered broker dealers and registered representatives, who, in FINRA arbitration typically prefer to disavow any fiduciary duty, (the highest standard of care) often to the surprise and detriment of retail investors. In certain cases despite broker’s push back, we have been able to uncover sufficient facts to support a claim for breach of fiduciary duty.

The gap between the SEC and FINRA’s investor protection measures give us yet another example of a disjointed regulatory & investor protection system. These same two regulators employing tens of thousands, highly skilled professionals each and jointly failed to catch scams such as Bernie Madoff and many others years after thousands of investors were damaged.

Blockbuster #2 Schwab is running major broadcast channel TV ads announcing a new S&P 500 index fund at 3 basis points compared to Vanguard’s 12 basis points. The competition is very healthy to see. Trustees and other fiduciaries involved should periodically compare trust account performance, not limited to return, risks, costs and expenses in comparison to the investment needs of the trust’s (and or other fiduciary account’s) purposes, terms, beneficiaries and cash flow requirements.

Blockbuster #3 the Fiduciary Rule has been partly in effect since last year, requiring FINRA – regulated stockbrokers to recommend investments in the customers’ best interest but the rest of it is still largely subject to SEC and or DOL and Congress review, changes and approval. See the recent Consumer Federation of America February 21 2018 letter to the DOL and SEC for an example why the rule should be in place now and this excerpt:

The [broker dealer’s] updated compliance manual stated that, “The firm does not use or rely upon quotas, appraisals, performance or personnel actions, bonuses, contests, special awards, differential compensation or other actions or incentives that are intended or reasonably expected to cause associates to make recommendations that are not in the best interests of Retirement Account clients or prospective Retirement Account clients.”

In fact, however, the firm ramped up its use of such contests, making no effort to exclude retirement accounts, according to Massachusetts’ well-documented complaint.

It allegedly set performance metrics and quotas for referrals to its investment advisory program, for example, that agents had to meet to qualify for certain prizes. And its “internal-use materials instructed agents to target a client’s ‘pain point’ and emotional vulnerability, while training sessions lauded the use of emotion over logic in getting a client to bring additional assets to the firm,” according to the complaint.

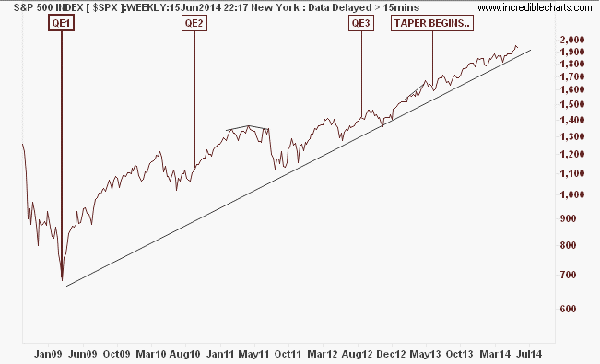

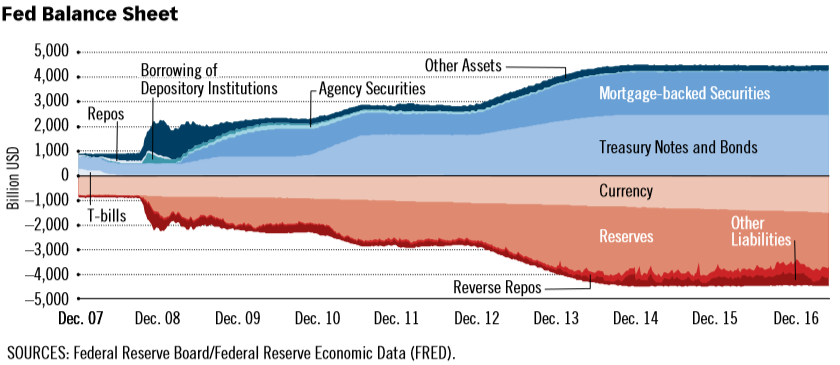

The set if you will forming a backdrop to the above includes: a recent new stock market high, record margin debt, followed by a still unexplained spike in volatility, as of February 5, 2018, a new Chairman of the Federal Reserve Board but not a new balance sheet against projected new US Treasury debt issuance of $1.5 Trillion in a real inflation-fueled, rising interest rate environment. The President’s recent surprise tariff talk may, to some, be a popular political theme, however if it were to become reality (it has), portends retaliation (see report that China targets Trump support base) and higher prices for US consumers feeding higher inflation. Interest rates’ Fed-induced somnolence may prove the undoing of 9 years under fake interest rates due to the Fed’s unprecedented quantitative easing aka the Large Scale Asset Purchase program.

The Fed announced 3 rate hikes for 2018, that’s not new news. And as of March 21 announced here. When they do raise, I wonder if they might announce on a billboard? That could be a cool new way to truly communicate to the masses!

What may be new news or perspective to some is the three card monty game going on in the US Treasury bond market including the Fed, the Primary Dealers including major broker / dealers and investors foreign such as central banks, sovereign wealth funds and private trusts and domestic such as hedge funds, investment companies better known as mutual funds, ETF’s, ERISA, Taft – Hartley (union) pension and retirement benefit plans, insurance and annuity companies and retail investors. Retail investors were listed last intentionally, as they are often the last to know and or act. Retail, HNW or so-called wealth management accounts include trusts, long the “stay-the-course” holders of “unsuitable often packaged long securities” may now see how the great QE experiment might play out for those who are less or late to act prudent, if at all and how this might end very badly; but just not for the first two participants in the shell game.

UNDERWATER HOMES / NEGATIVE EQUITY AS OF 3Q 2018

Academics refer to this as ‘information assymetry,” in street terms what you don’t know, which others know, can and may hurt you. Information assymetry, information held almost exclusively by the five CSE’s, certain other large east-of-the-Hudson banks’ SIBHCs pursuant to the SEC’s ill-advised (SEC hearing on April 28, 2004 to termination by Chairman Cox effective September 26, 2008) CSE program, AIG and certain regulators caused the GFC (Great Financial Crisis). Millions of homeowners were lured into a fraudulent housing market and lost their homes, life savings and more. Millions more are still underwater on their mortgages. That’s how real and dangerous information assymetry was, still is and can be.

According to CoreLogic, from the second quarter of 2018 to the third quarter of 2018, the total number of mortgaged homes in negative equity decreased 4 percent to 2.2 million homes or 4.1 percent of all mortgaged properties. Year over year, the number of mortgaged properties in negative equity fell 16 percent from 2.6 million homes – or 5 percent of all mortgaged properties – in the third quarter of 2018.

Trustee’s often are led to believe (in practice they are often SOLD on the idea) they can delegate and get a free pass on responsibility if things go wrong.

Trustees and investors and retirees (including spouses during marriage and while going through divorce) in general may need a reminder that accounts, especially many of those at broker dealers are NOT opened as fiduciary standard, but as suitability accounts, a lesser standard. When trustees get into arbitration the unpleasant surprise and misgivings run deep and are often a little too late. Fortunately, with expert testimony and or pre-hearing consulting we have helped to elucidate the applicable standard of care.

Trustees and fiduciary agents selected by the trustee to assist the trust such as banks, brokerage firms, stockbrokers, financial advisers, financial planners, life insurance and annuity agents, sometimes CPA’s and lawyers fall under the zone of fiduciary duty to the trust and beneficiaries subject to the best interests and prudence tests, among others.

In so many words, that test is going on now, trustees waiting or hoping to cram, paper over or pass it at the last minute will not be viewed kindly by beneficiaries, the opposing spouse in divorce, courts or FINRA arbitration panels, given the potential, foreseeable volatility that’s on the horizon. And we haven’t even brought up Special Counsel Mueller’s ongoing investigation, potential gun legislation, the historic March 14 nationwide high school walkout, the 2018 mid-term elections here in the US, the recently enacted Tax Cuts (both the benefits and costs short, medium and long term thereof), Climate change’s explicit and implicit costs, Minimum wage 50% increases (California’s is going from $10 to $15 per hour by 2022), Fake news, Brexit, Russia’s US and worldwide election meddling tactics (and not that they were or are the only ones doing it) and new long range stealth nuclear weapons announcement, North Korea’s nuclear ambitions and the ubiquitous and uncontrollable cyber-hacking.

March 16, 2018 update

Blockbuster #4 was announced yesterday. iHeart Radio whose corporate name is iHeartMedia, the largest US radio station operator (858 stations including the three largest in Los Angeles) came out with a bankruptcy filing (excluding its Clear Channel billboard units) including a pre – cooked mammoth restructuring of $20 Billion in debt, reducing it by $10 Billion.

Ripple Effects

This suggests as previous such multi – billion dollar bankruptcies, the entire media industry’s economics may have changed in a stroke of the pen including potentially all forms of media. While the company has been known to be struggling since 2016, it raises several flags of caution to prudent investors and fiduciaries to witness a large diverse group of hundred of radio stations with no inventory or physical plant assets, suffer under crushing debt and punish shareholders and bondholders, iHeart shares last traded on the NASDAQ pink sheets for 48 cents. Further, the hits taken by investors and bondholders are not usually soon forgotten, future deals will placed under tighter scrutiny, with potential ripple effects across ALL industries and even extending to the counterparties of the iHeart investors and bondholders not limited to banks, hedge funds, private equity firms, mutual funds, and ETF’s. Ratings agencies such as S&P, Moodys, Fitch and others will, as they should have been, potentially issuing ratings alerts and or negative guidance on current and future ratings on companies shares or debt which may be connected to the iHeart filing.

One last thing, the next time you open an app on your smartphone or iPhone to buy something, implicitly you are using the app because in part you find it to be faster, better, cheaper and or more convenient; many of the same qualities you as a trustee or fiduciary should be thinking about and acting upon when it comes to prudently managing a trust, involved in a divorce or any other fiduciary account.

For questions or assistance please email info@fiduciaryexpert.com or call (310) 943-6509

Copyright Chris McConnell & Associates 2018 All rights reserved